The macro environment is more volatile, unpredictable and complex than ever. Not only due to the severity of the multitude of global events, but also due to the complexity of these events happening at the same time.

The key question is: what happens to liquidity when the following standalone events collide?

- A global pandemic causing supply chain collapses and raw material supply shortages

- A “war on energy” causing historically high supply shortages of energy

- A soaring inflation which will most likely trigger a recession in the world economy; it is only a matter of how big a recession

- Rising interests rates to mitigate inflation directly and negatively impact the cost of capital

- Not to mention the general global political polarisation and China’s interest in Taiwan

The list goes on, and the consequences, however difficult to predict, are many. Based on conversations with top management of industrial companies in Denmark, this article explores the consequences of the above-mentioned events and discusses one performance metric in particular that deserves more focus in these uncertain times.

Having a strong working capital and a strong cash/capital structure can prove vital in the coming years.

The pandemic and Russia’s war in Ukraine have caused major issues to global supply chains, we have seen record-high inventories and working capital levels across most industries. The growing inventory has generally been regarded as a safeguard buffer to ensure a high service level in the deliveries for customers.

In an environment where you continue to generate strong cash flows, the equation holds.

The fact that inflation and cost pressures have reached a 30-year high and the US has had two back-to-back quarters of negative GDP growth indicates but one thing. A recession is brewing, and this time, natural inflation is keeping the central banks from solving it with a “money printer”. To counter inflation, interest rates must stay high or go higher which will result in an economic slowdown.

That means no growth, less cash flow, unpaid debt and bankruptcies.

With this outlook, it is a serious concern that the general development over the last couple of years across industries has been a clear build-up of cash tied up in operations. High inventory levels proved to be the perfect counter-response to the pandemic, but already now, that “strategy” can prove outdated and very expensive.

Some inventory build-up strategies that worked under the pandemic now pose a great cash liability.

Several industries, such as retail, e-commerce and consumer goods, are already experiencing major issues with rampant price levels and problems in the value chains. After a long period of cheap and accessible capital, many companies now experience increasing challenges in raising sufficient financing to sustain growth or even to continue operations. However, a source of financing that is often overlooked in times of low interest rates is to increase internally supplied funds through more efficient utilisation of working capital.

The tie-up of capital is increasing across markets all over the world. Below, we showcase the Nasdaq Nordic MidCap segment and how working capital levels expressed in days have developed across the last five and a half years. Unsurprisingly, the development of the number of days of inventory shows that the Danish industrial companies, like several other companies and industries in the world, have built up substantial buffer stocks during the pandemic. It is noteworthy that even before the pandemic, there was a clear trend of deteriorating inventory turnover.

The current acceleration in the stock build-up may suggest a “bullwhip effect” related to supply bottlenecks. In an environment characterised by high demand and uncertainty about the supply of inputs, firms tend to hoard inventories of inputs beyond actual needs as a precaution. This so-called bullwhip effect might have led to an amplification of the procyclicality of changes in inventories in the present environment. This can partly be explained by the fact that over a longer period, companies focused on growth and ensuring deliveries in a simple way.

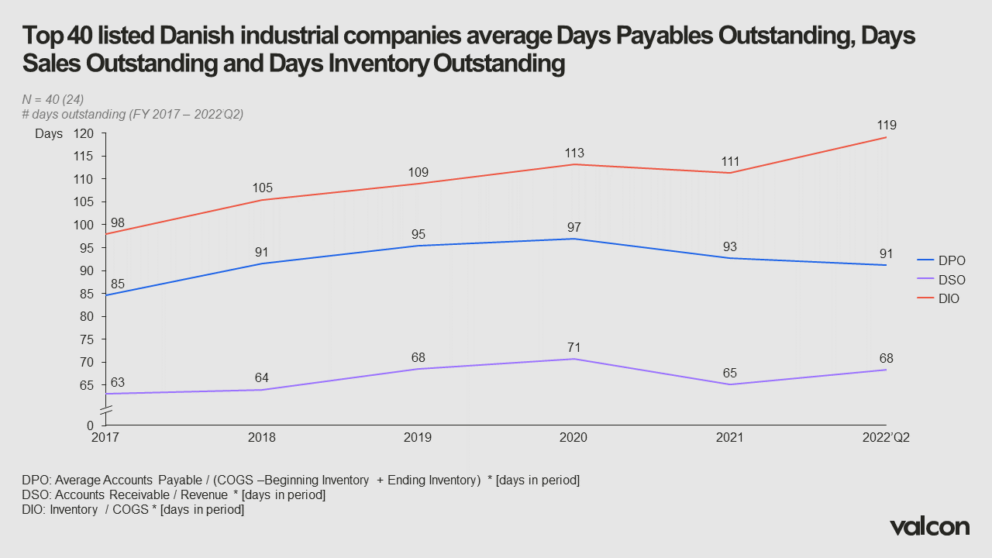

If we look at the 40 largest listed Danish industrial companies (measured on revenue), the trends are even more evident. These companies are chosen as they reflect the type of companies that would be more prone to the before-mentioned events. From 2017 to 2022 Q2, the net working capital increased by 26% from 76 days to 96 days. This increase is substantial and is currently trending upwards.

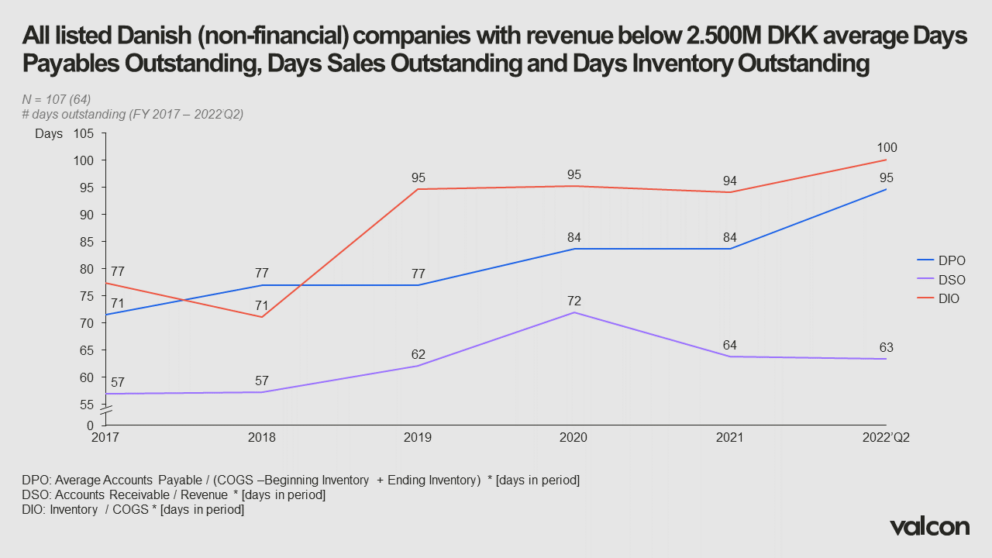

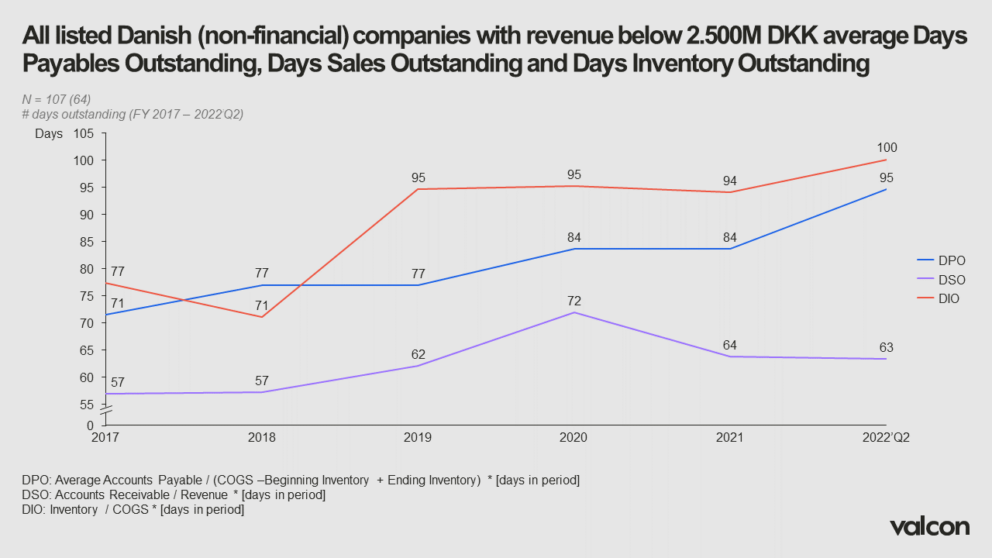

If we look at all non-financial Danish companies below 2.5b DKK, an interesting observation can be made. Days payables outstanding has seen a steady increase with an immense 13% hike up in 2022 isolated. This hike and general level is a rare sight under normal circumstances, and it could indicate an increasing proportion of companies struggling to pay on time, which resonates with what we are experiencing in the market.

When prices for input goods, electricity and transport increase at the same time as demands for wages, margins are likely to be put under pressure. More and more signs also point to an increased risk of a slowdown in the economy, which further emphasises the importance of paying close attention to tied-up capital, cash flow and debt levels going forward. It becomes increasingly critical for companies to review their working capital and free up liquidity by becoming more capital efficient.

In conclusion, an inventory build-up strategy combined with highly volatile and increasing prices puts a severe strain on the companies’ capital to run operations. In combination with the fact that interest rates have increased dramatically, which generally increases the cost of capital, we come up with expressions like “a dangerous working capital cocktail”.

More money is being tied up in operations, and unfortunately, it no longer comes for free.

Want to learn more? If you want a benchmark on the state of the nation of your working capital, please email Lasse Kobberup ([email protected]) or Richard Thorsen ([email protected]) and we’ll be in touch right away.